Risk does not disappear, it changes location

In financial markets, risk rarely disappears. Often, it simply changes location. This idea helps explain one of the most important transformations in the Brazilian market over recent years: the gradual migration of corporate financing from bank balance sheets to the capital markets.

In many respects, this evolution is positive. Deeper capital markets expand companies’ sources of financing, reduce dependence on the banking system, lower systemic risk, and allow long-term projects to connect with investors whose investment horizons are better aligned with their duration. Yet the same transformation that broadens opportunities also redistributes risks. When credit ceases to be concentrated on bank balance sheets and becomes directly funded by the market, defaults and restructurings begin to affect the portfolios of institutional investors, funds, and families more directly.

In this letter, we review the recent trajectory of private credit in Brazil, its origins, the disintermediation process, the growing participation of retail investors, and the first major default events directly affecting this investor base. We compare the local landscape with international experience and reflect on the incentives shaping the various participants across the credit chain. Finally, we present Turim’s perspective on how to navigate this new phase with the discipline it demands.

Disintermediation Gains Scale

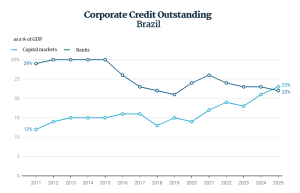

By the end of 2025, the capital markets had surpassed banks as the primary source of corporate credit in Brazil. Corporate credit outstanding through the capital markets reached approximately 23% of GDP, while bank lending to companies represented roughly 22%. The difference is small in magnitude but significant in meaning: it signals that Brazilian corporate financing has entered a new phase.

Source: Central Bank of Brazil and ANBIMA / Prepared by Rio Bravo

International comparisons help illustrate the potential path still ahead. In more mature markets, particularly the United States — despite its own structural specificities — corporate credit via capital markets represents approximately 51% of GDP, while banks account for around 9% of GDP in corporate lending. The figures vary across countries, but the direction is consistent: as financial markets mature, the role of bank balance sheets in corporate financing tends to decline.

This disintermediation brings meaningful benefits. Companies gain access to more diversified funding sources; investors can access instruments with different maturities, indexers, and risk profiles; and long-term projects find financing channels better suited to their development cycles. However, the shift also transfers part of the analytical responsibility — previously concentrated within the bank credit desk that originated and held the risk — to a much broader base of end investors.

In other words, the maturation of capital markets also requires the maturation of their participants. The more corporate financing migrates toward end investors, the greater the importance of independent processes of analysis, selection, diversification, and ongoing monitoring.

Infrastructure Debentures: A Case Study of the Transition

Infrastructure debentures are perhaps the clearest example of this transition. Brazil faces a structural need for infrastructure investment, while the public sector and development banks operate under fiscal, regulatory, and balance-sheet constraints. Against this backdrop, capital markets have increasingly assumed a larger role in financing long-term projects.

Created under Law 12,431/2011, incentivized debentures were designed to finance projects deemed strategic, offering income tax exemptions for individual investors and creating a direct channel between private savings and productive investment. The replacement of the TJLP by the TLP in 2018 proved fundamental, as it brought BNDES lending costs closer to market rates and reduced the implicit subsidy embedded in public credit, thereby enabling greater market participation in financing the sector.

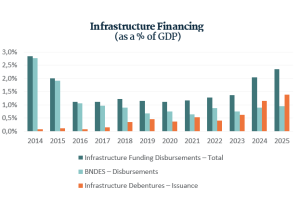

The data illustrates the transformation. In 2014, BNDES disbursements for infrastructure represented approximately 2.8% of GDP, while infrastructure debenture issuances accounted for less than 0.1% of GDP. By 2025, the picture had changed substantially: infrastructure debenture issuance reached approximately 1.4% of GDP (around BRL 178 billion), surpassing BNDES disbursements to the sector, which stood near 1.0% of GDP (BRL 121 billion).

This shift demonstrates that infrastructure debentures have evolved from a complementary instrument into a central pillar of long-term project financing in Brazil.

Source: BNDES and ANBIMA

Even so, the growth opportunity remains significant. Estimates suggest that infrastructure investment in Brazil should reach between 4% and 5% of GDP in order to reduce historical bottlenecks and sustain a more robust growth trajectory. Given the State’s fiscal limitations and the balance-sheet constraints faced by public banks, it is reasonable to expect that a substantial portion of this financing will continue migrating toward the capital markets, with the potential for issuance volumes to double relative to current levels.

The New Frontier: Retail Investor Participation

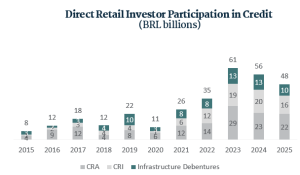

The expansion of private credit has also brought a significant change in the investor base. Individual investors, who historically accessed corporate credit primarily through investment funds, began purchasing incentivized debentures, CRIs, and CRAs directly through investment platforms.

The numbers highlight the magnitude of this shift. Based on ANBIMA data, the average annual direct participation of retail investors in CRA, CRI, and infrastructure debenture issuances was approximately BRL 45 billion between 2021 and 2025, compared to around BRL 24 billion between 2016 and 2020 — representing growth of approximately 91% between the two five-year periods.

Source: ANBIMA – Capital Markets Bulletin

This popularization changes the nature of the risks assumed by individual investors. When an individual purchases a bank deposit certificate (CDB), the investor assumes the credit risk of a financial institution and, in many cases, benefits from FGC protection within applicable limits. When directly purchasing a debenture, CRI, or CRA, however, the investor assumes corporate credit risk, structural risk, liquidity risk, and, in some cases, project or collateral execution risk.

The democratization of access to private credit has, in many respects, been a positive development. Yet democratizing access is not the same as democratizing analytical capability. And it is precisely within this gap — between purchasing a product and fully understanding its risks — that many problems emerge.

When Risk Materializes

The first years of this new phase in Brazilian private credit have already produced episodes worth noting. Rodovias do Tietê entered judicial restructuring in 2019 and was among the first cases to affect a more representative base of investors. The debt involved totaled around BRL 2 billion, with approximately 15,000 individual investors directly exposed.

More recently, in 2026, the Raízen case illustrated a significant increase both in financial magnitude and in the number of affected investors. The company, one of Brazil’s largest agribusiness groups, filed for out-of-court restructuring involving approximately BRL 11.4 billion in debentures and CRAs, with nearly 120,000 taxpayer IDs exposed.

The episode is instructive for two reasons. The first concerns the role of credit ratings. In the domestic market, the company held a AAA rating from rating agencies — the highest category of credit quality. Internationally, it carried an investment-grade rating above Brazil’s sovereign rating. Nevertheless, Raízen had already been showing a progressive deterioration in margins across consecutive harvest cycles, pressured simultaneously by lower international sugar prices, rising costs, and increasing leverage.

The second point is subtler and closely related to the first. Much of the market’s confidence in the structure rested on an implicit assumption: that the profile of the controlling shareholders —Cosan and Shell— would itself provide additional support in a stress scenario. The issue is that this type of support evolves over time and depends on economic incentives— financial considerations may lead controlling shareholders to prefer debt renegotiation rather than injecting fresh capital into the company.

Our main takeaway from this case is that even credits supported by strong external ratings require independent and continuous monitoring. Conditions change both from a microeconomic perspective — such as commodity cycles or competitive dynamics within an industry — and from a macroeconomic perspective, such as the increase in Brazil’s Selic rate from 2% per year in 2020 to 15% in 2025. Ratings remain important inputs, but they ultimately reflect a snapshot of the past and assumptions that may later prove invalid.

These cases should not be interpreted as arguments against private credit. On the contrary: mature markets coexist with credit cycles, restructurings, and losses. The key point is that, as the market grows, such events cease to be peripheral exceptions and become part of the natural process of risk selection. Investors participating in this asset class must be prepared to live with this reality. Credit analysis does not end with the investment decision; it merely begins there and only concludes once the credit has been fully repaid.

The 5 Cs Applied to the Brazilian Reality

Credit analysis is often summarized through the so-called 5 Cs: character, capacity, capital, collateral, and conditions. The framework is old and simple in formulation, yet precisely for that reason it remains useful — because it forces investors to look beyond the yield being offered. In Brazil’s current context, each of the five deserves closer attention.

Character refers to the quality of the borrower: track record, governance, transparency, and willingness to honor commitments. This means evaluating shareholders, management, boards of directors, dividend policies, prior relationships with creditors across different cycles, and the quality of audited financial statements. In credit, issuer quality rarely appears in a single metric; it reveals itself through the accumulation of decisions made over time.

Capacity evaluates cash generation and the ability to service debt over time. The relevant exercise here is stress-testing assumptions: can the issuer continue servicing debt if profitability falls 20% below projections? What if interest rates remain elevated for longer? What if access to the capital markets temporarily closes?

Capital examines financial structure, leverage, and balance-sheet resilience. Net debt-to-EBITDA ratios and covenants are merely the starting point. Investors must also analyze debt composition by maturity and indexation, unhedged foreign exchange exposure, the investor’s position within the capital structure — whether senior, mezzanine, or subordinated — and, when applicable, regulatory capital levels. Together, these elements help determine the issuer’s true financial resilience and the actual risk profile of the instrument.

Collateral concerns guarantees and their effective recovery value under adverse scenarios. In private credit, the priority structure among investors can be as important as the financed asset itself. Senior, mezzanine, and subordinated tranches carry very different risk profiles: the senior tranche has priority in receiving cash flows; the mezzanine tranche occupies an intermediate position; and the subordinated tranche absorbs first losses. The same receivables portfolio can therefore produce materially different risk profiles depending on the investor’s position. Evaluating collateral requires understanding not only the value of guarantees, but also payment priority, effective subordination, and the actual recovery capacity under stress scenarios.

Conditions incorporate the macroeconomic, sectoral, regulatory, and competitive environment. Historically compressed credit spreads rarely coincide with improving fundamentals — more often, they reflect excess demand relative to supply rather than genuine reductions in risk. The cycle matters, and it matters increasingly as the market deepens.

Private credit demands a particular form of humility: recognizing that not all risks are measurable, not all collateral is enforceable, and not every well-rated issuer today will remain a good borrower tomorrow. Apparently attractive yields rarely compensate for permanent capital losses. In many cases, the best investment decision is simply not to participate in an offering — or not to hold a given risk exposure.

Incentives: The Invisible Variable

“Show me the incentive, and I will show you the outcome.”

Charlie Munger

To understand market decisions, it is essential to understand how participants are compensated. In private credit, this lens is especially revealing because the chain between issuer and end investor involves multiple intermediaries, each operating under its own incentives — which are not always aligned.

Let us begin with the issuer. Companies naturally seek to present the most favorable possible scenario in order to raise capital at the lowest cost. There is nothing inherently wrong with this; it is part of the CFO’s role. But it also means that testing management narratives through comprehensive financial analysis is prudent and necessary — in practice, this is precisely the exercise embodied in the 5 Cs.

Rating agencies have operated for decades under the so-called issuer-pays model, whereby the issuer pays for the rating. This arrangement came under intense scrutiny following the 2008 financial crisis, when overly optimistic ratings assigned to U.S. mortgage-backed structures contributed to the scale of losses. The model was not replaced, but institutional investors learned to treat ratings as one input among many — not as definitive conclusions.

Finally, there is the distribution chain. In distribution-based models, intermediaries may be incentivized through commissions, placement fees, or other forms of compensation linked to fundraising success. Potential conflicts emerge when different products generate different economic returns for participants along the chain: in such contexts, there may be incentives to prioritize products that better compensate the distributor, rather than those best aligned with the client’s interests.

The key point is transparency around incentives. What matters for end investors is recognizing them and understanding where misalignments may arise. In credit, poorly aligned incentives can be particularly costly because mistakes tend to surface only later. Distribution compensation occurs at issuance; the realization of risk may occur years afterward. This time lag makes the separation between product distribution and wealth management even more important.

Regulatory Transparency and the Independent Compensation Model

CVM Resolution 179 represents an important step forward in this discussion. We addressed its implementation in our Letter 43 (May 2025), when discussing how time exposes previously hidden fragilities within management structures. Here, we revisit the regulation through a different lens: information asymmetry within the distribution chain, which becomes more visible as credit assets encounter stress.

The new rules expand transparency for investors: institutions must now provide quantitative disclosures regarding compensation received from the distribution of securities, through quarterly statements. The objective is to allow clients to understand how much institutions or intermediaries receive as a result of their investments and, consequently, better assess potential conflicts of interest. Particularly high placement commissions should naturally draw investors’ attention. Regulatory progress does not eliminate conflicts, but it makes incentives more visible — and visibility itself is part of the solution.

The structural counterpoint is the fee-for-service model, under which clients directly compensate for advisory, analysis, monitoring, and portfolio construction services. Separating wealth managers’ compensation from financial product distribution mitigates conflicts and reinforces investment independence. The logic is straightforward: the client compensates the management of wealth, not the placement of a specific asset.

In private credit, this distinction is especially important. Since returns are generally capped at the contracted carry, while potential losses may be permanent, alignment of interests becomes even more critical. An independent compensation model allows alternatives to be compared on more transparent grounds, enables genuinely independent analysis of structures, and, when necessary, supports saying “no” to transactions offering apparently attractive yields but inadequate risk-return dynamics.

The Discipline of Avoiding Losses

The development of Brazil’s private credit market is both positive and necessary. It expands corporate financing, supports long-term projects, and offers investors meaningful alternatives for diversification and return generation. But credit should not be treated as a mere extension of traditional fixed income. Credit is, at its core, the analysis of permanent capital loss risk.

Howard Marks of Oaktree describes the required discipline succinctly. In his memo Fewer Losers, or More Winners?, Marks argues that, across many investment segments, strong long-term performance depends less on identifying major winners and more on avoiding major mistakes. Investing in credit is often described as a negative art — the art of excluding issuers and structures that may produce permanent losses. The upside of a debt instrument is generally limited to the repayment of principal and interest; the downside, by contrast, can impair a meaningful portion of capital. Small differences in selection, compounded over time, produce large differences in outcomes.

The Brazilian market will continue evolving. Companies will continue seeking alternatives to bank credit; infrastructure will continue demanding private capital; and retail investors will continue accessing products directly. But this growth must be accompanied by diligence, independence, and proper incentives. The three must evolve together.

In our first Turim Letter, written more than two decades ago, we described our purpose as “to protect, preserve, and grow the wealth” of the families and institutions that entrust us with this responsibility — in that order. In private credit, that sequence matters especially. Our role is not to pursue credits with the highest apparent yields, but rather to select those that fit within a wealth strategy aligned with the interests, objectives, and time horizon of our clients.

Preserving capital is not a defensive posture. It is the first condition of any legacy intended to endure across generations — and therefore the essence of disciplined credit investing.

References

- ANBIMA. Capital markets data, incentivized debentures, CRAs, and CRIs. 2025.

- BNDES. Infrastructure financing disbursement data. 2025.

- BRAZIL JOURNAL. Raízen CRAs: where the knife stops falling. 2026.

- ESTADÃO. Infrastructure reaches record investment levels but still faces a multi-billion-dollar deficit.

- ESTADÃO. Capital markets surpass banks in corporate lending for the first time in history. 2026.

- INVESTNEWS. Meeting of Raízen CRA investors. 2026.

- MARKS, Howard. Fewer Losers, or More Winners? Oaktree Capital Management, 2023.

- VALOR ECONÔMICO. Creditors fear the end of the Rodovias do Tietê concession. June 11, 2019.